A guide for directors navigating a company in financial distress

In today’s economic and geopolitical landscape, businesses can rapidly find themselves in challenging financial situations. Navigating periods of financial distress requires an understanding of the legal landscape. This guide provides directors guidance on how to act responsibly and diligently in such situations and mitigate liability risks.

By Bas van Voorst

Expertise:

Dispute Resolution

03.03.2026

1. PRINCIPLES OF PROPER MANAGEMENT

The board (bestuur) of a Dutch limited liability company (besloten vennootschap, bv) is responsible for managing the company. What this entails, depends on the nature, size and internal policies of the company and the circumstances in which it operates. In any case, managing the company means setting, executing, and adjusting the company’s strategy and keeping risks in check. Although the board is accountable to the general meeting (algemene vergadering) and the supervisory board (raad van commissarissen), directors are generally afforded a large degree of policy freedom on business decisions. Amongst others, this means directors are permitted to take responsible risks.

The board must act in the best interest of the company and its enterprise. In general, the interest of the enterprise is best served by promoting the long-term success of that enterprise and aiming for long-term value creation. Additionally, the board must also exercise due care towards the interests of all other stakeholders involved with the company and its enterprise, to ensure their interests are not unnecessarily or disproportionally harmed. Important stakeholders include employees, suppliers, customers, creditors, and shareholders. In the next few paragraphs, we will explain how these principles apply when a company goes through financially challenging times.

2. PHASES OF FINANCIAL DISTRESS

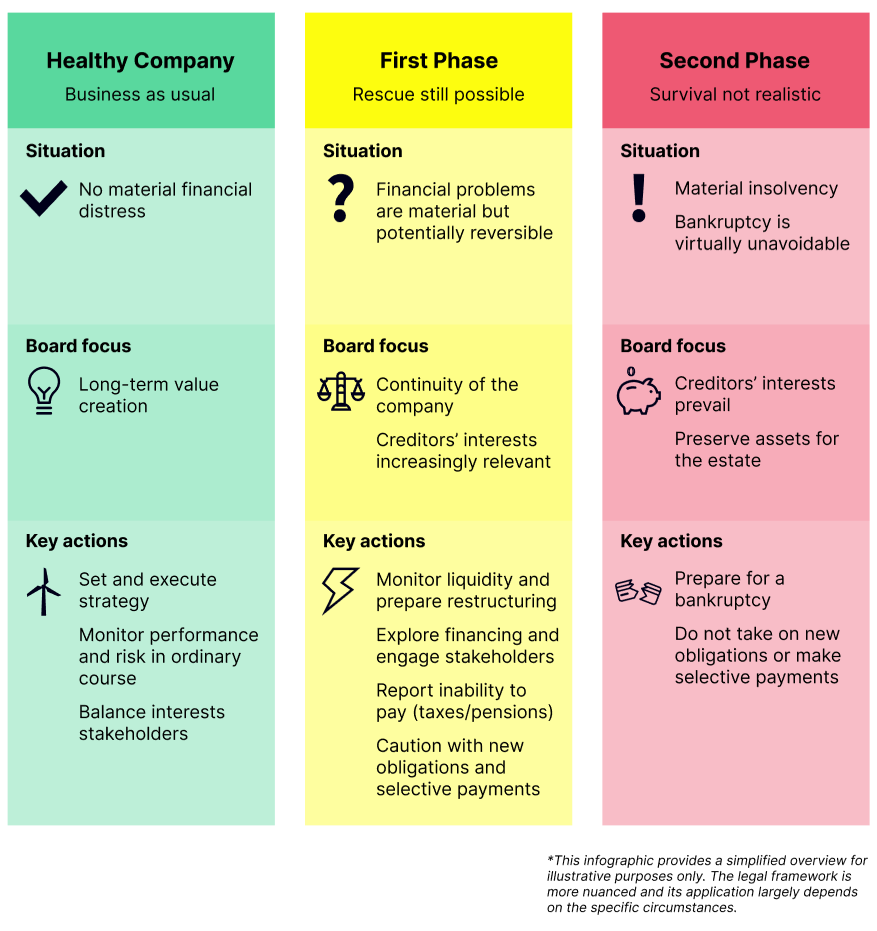

When a company enters financial distress, the board's duties intensify and require a stricter standard of conduct and the interests that the board needs to prioritise shift. The exact duties and limitations of the board depend on the level of the financial distress. This may be categorised into two phases.

The first phase is characterised by concerning financial developments, but where timely and adequate intervention could still secure the company’s continuity. In this phase, the board can still realistically uphold the position that the crisis situation is reversible. This can, for example, be the case if there are still ongoing discussions with potential investors or credit providers, and there is a real chance that, if such investment or credit is obtained, the company can turn things around financially. This situation requires adequate action and sometimes difficult decisions from the board. However, the board’s primary focus can remain on long-term value creation and the sustained success of the enterprise.

The second phase is reached when the company is materially insolvent, and it becomes clear that it will not realistically have a chance of survival. In other words: the financial crisis is irreversible. As soon as the board knows or reasonably ought to know that the company’s bankruptcy is virtually unavoidable, the interest of the joint creditors prevails, and the board must shift its focus to the preservation of assets in the interest of the joint creditors. This requires a fundamental shift in the board’s responsibilities.

3. PROPER MANAGEMENT IN THE FIRST PHASE

In the initial phase of financial distress, the board remains primarily focused on safeguarding the continuity of the company and its long-term value creation. Even though creditors have accepted the entrepreneurial risk of non-payment, the board must increasingly consider their interests. This requires careful monitoring of the company's financial condition to determine whether it is still in the first phase or has entered the second phase.

In the first phase, the board must act proactively to address financial challenges and explore viable solutions. In our experience, companies often delay action due to over-optimism or competing priorities. Three categories of recommended action are as follows:

Implementing cost-saving and operational measures to stabilise the company’s cash position. This may include stretching payment terms, pausing non-core activities or investments, and tightening debtor and creditor management. For this purpose, it is essential that the company implements strict cash flow management and continuously updates its cash flow projections.

Developing and initiating a strategic restructuring plan based on a thorough assessment of the company’s financial and operational position. This may involve renegotiating debt and engaging early with key stakeholders to build support for proposed measures.

Exploring internal and external financing options to strengthen liquidity, extend the financial runway, and discuss these options with potential investors and stakeholders. This may include securing bridge loans, equity-based financing, or generating cash internally through asset sales.

To sum up, the company needs to know and attempt to extend its runway and use that runway to explore financing or restructuring options. Generally, the board of the company will be in the lead in determining and executing these actions. Depending on the company’s governance structure and the nature of the measures contemplated, this may also require timely involvement of the general meeting of shareholders and/or the supervisory board.

3.1 Caution with new obligations

A key consideration starting in the first phase, is whether the company should still assume new obligations. Entering into new obligations, for example with new suppliers, is often essential for the continued survival of the company. However, there is also a growing risk that the company will not be able to comply with its new obligations.

Directors can be held personally liable if they incur new obligations on behalf of the company while knowing or reasonably having to know that the company would not be able to meet its obligations and would not offer recourse for the damages. During the first phase, this high threshold of liability is usually not met, as there is still a realistic chance that the financial distress is turned around. However, if such outlook does not exist, the company has entered the second phase, and it could be considered unlawful to enter into new obligations.

A potential solution to avoid liability under this standard, is to fully inform new creditors about the company’s financial situation, so that the creditor can assess if they want to accept this risk. Of course, we understand that in practice disclosing the financial distress is often not desirable from a commercial perspective.

3.2 Caution with selective payments

If the company is in a healthy financial situation, the board has – within reason – the policy freedom to make strategic choices to decide which creditors it prioritises, without the risk of directors’ liability. In times of financial distress, when the company lacks sufficient funds to satisfy all creditors, this discretion of the board becomes more limited, and directors should become more diligent and considerate – and realise that soon they may need to start treating creditors in accordance with the relevant legal ranking, meaning the legally prescribed order in which creditors must be paid in the event of bankruptcy.

A director may be held liable if they knew or should have known that their actions would result in the company failing to meet its obligations and the company does not offer any recourse. Again, this is a high threshold. Especially in the first phase, selective payments may be permitted if the circumstances and the company’s interest that the board needs to consider justify such preferential treatment. For example, prioritizing paying employees or key-suppliers may be necessary to avoid shutting down, which ultimately is in the interest of the enterprise and the joint stakeholders.

If the company reaches the second phase, it will generally be more difficult to justify selective payments as the board’s focus shifts from the continued survival of the company to the preservation of assets for the creditors. Also, in this phase it is more likely that creditors remain unpaid. Therefore, in the second phase, selective payments are generally no longer allowed, except insofar as these selective payments benefit the collective creditors.

3.3 Preventing fraudulent acts in respect of creditors

In addition to the risk of directors’ liability, there is a risk that in a bankruptcy, the bankruptcy trustee (curator) annuls certain legal acts performed prior to the bankruptcy if they are fraudulent in respect of creditors on the grounds of actio pauliana. These limitations become especially relevant in the first and second phase, as a bankruptcy becomes a realistic scenario and companies often look for creative ways to restructure their business and shield certain stakeholders (such as new investors) from the risk of a bankruptcy. There are two categories of legal acts that can be annulled on these grounds:

Non-obligatory acts whereby both the company and the counterparty knew or should have known at the time it was performed that it would harm the interest of the creditors because a bankruptcy and a deficit in the bankruptcy were foreseeable. For certain transactions, such as acts without (real) consideration, acts that are not due or transactions with certain affiliated parties, knowledge of the counterparty is presumed if the actions happened within one year prior to the bankruptcy.

Obligatory acts if the counterparty knew that the company had already submitted its bankruptcy application or if the payment was the result of collusion between the company and the counterparty with the aim to give the counterparty a preferential treatment over other creditors.

From the perspective of the board, this means that particular caution is required when entering into transactions in the vicinity of insolvency. The board should critically assess whether a contemplated transaction is obligatory or discretionary, whether it could disadvantage the joint creditors if bankruptcy were to follow, and whether it may be perceived as granting preferential treatment. Transactions with affiliated parties, transactions without adequate consideration, or payments that are not yet due, require heightened scrutiny. In all cases, the board should ensure that the commercial rationale of the transaction is sound and carefully documented, so that it can be justified if subsequently reviewed in bankruptcy.

3.4 Reporting inability to pay

The company is obliged to inform the Dutch Tax Authorities (Belastingdienst) of its inability to pay certain taxes. This notification must generally be submitted within two weeks after the due date for payment. Additionally, the company must provide any further information or documentation requested by the Dutch Tax Authorities.

If a timely and correct notification is made, directors are only personally liable if it is plausible that the non-payment of taxes resulted from improper management attributable to them, occurring within the three years prior to the notification. However, if no timely and correct notification is made, each director is jointly and severally liable for the unpaid taxes (including possible penalties and interest). In that case, it is presumed that the non-payment is due to the director’s fault, and the burden is on the director to plausibly demonstrate that the failure to notify and the non-payment are not attributable to them.

A similar notification obligation and corresponding directors’ liability risk apply to contributions to sector-wide pension funds.

3.5 Relationship with other bodies and persons

In the early stages of financial distress, the role of shareholders and the general meeting of shareholders typically remain limited. However, depending on the type of company and its shareholders, it may be beneficial to keep them informed and involved –for example to reduce the risk of disputes, use them as a sparring partner, and to explore internal financing options. If there is a real threat of the company entering into the second phase, the board should increase its efforts to inform the shareholders and the general meeting of the financial situation, so that the shareholders have sufficient information if they do have to decide on the bankruptcy of the company.

If the company has a supervisory board, cooperation between the board and the supervisory board should intensify in the first and second phase. While the supervisory board generally advises and supervises the board, a worsening financial situation calls for a more proactive and supportive role. The supervisory board must closely monitor the company’s financial condition and the board’s actions and intervene when necessary. To enable the supervisory board to assume this responsibility, the board must share all relevant information proactively and on an ongoing basis.

Depending on the company's trajectory and restructuring plans, the board should consult with the works council (ondernemingsraad). Additionally, the board must assess whether the new financial situation and the envisaged actions are subject to contractual provisions, such as information, consultation of approval rights under its governance or financing arrangements.

3.6 Documentation and record-keeping

Especially starting in the first phase of financial distress, careful documentation of the board’s considerations and decisions is of paramount importance. As the company’s financial position becomes more vulnerable and the interests of creditors gain prominence, board decisions are more likely to be scrutinised at a later stage, for example in the context of directors’ liability claims or bankruptcy proceedings. It is therefore essential that the board properly records the financial information on which it relies, the alternatives it has considered, the interests it has weighed and the reasons why certain measures were deemed to be in the interest of the company and its stakeholders. This applies in particular to decisions relating to the assumption of new obligations, selective payments, restructuring steps, financing arrangements, and transactions with affiliated parties.

Proper record-keeping serves multiple purposes. Internally, it promotes disciplined decision-making and enables effective supervision by the supervisory board and, where relevant, accountability towards shareholders. Externally, it may provide crucial evidence that the board acted in an informed, diligent, and reasonable manner, and that it continuously assessed whether the company was still in the first phase. In a situation where hindsight may colour the assessment of past conduct, contemporaneous documentation can be decisive in demonstrating that the board fulfilled its duties responsibly and in the best interest of the company and its enterprise.

4. PROPER MANAGEMENT IN THE SECOND PHASE

If the actions of the board during the first phase do not have the required effect, it is possible that at some point there is no longer a realistic chance of the company’s survival. In this second phase, when the board knows or reasonably should know that the company’s insolvency is virtually unavoidable, the board’s focus should shift from long-term value creation to preserving value for its collective creditors.

4.1 No new obligations or selective payments

Due to the prevailing interest of the creditors, and the lack of future prospect for the legal entity, there is not much room for the company to enter into new obligations, as the board should reasonably know that the company will not be able to meet its obligation, or provide recourse. The same goes for making selective payments, as these will generally not benefit the collective creditors and may disproportionately harm the interests of creditors. As a general rule, entering into new obligations and making selective payments are no longer allowed in the second phase and carry the risk of directors’ liability, unless the board can adequately justify those actions based on the specific circumstances and interests.

For example, a generally accepted example where these actions can be justified is the hiring and payment of outside counsel to advise on the appropriate course of action and assist with the necessary arrangements. This counsel could also assess the possibilities of a creditors’ settlement to avoid bankruptcy or the viability of a restart out of bankruptcy. Engaging counsel and prioritizing their payment could be in the best interest of the enterprise and its stakeholders (such as creditors, employees, and customers). There are also other examples where a relatively small payment by the company would result in a larger benefit for the company’s assets (and the bankruptcy estate) and therefore benefit the collective creditors. With regard to these payments, the board should also consider whether the payment needs to be made immediately, or whether it is possible and more appropriate to leave such a decision up to the bankruptcy trustee.

4.2 Prepare for bankruptcy or suspension of payments

In practice, the winding down of the business and the preservation of value for creditors generally follow these steps. In this guide we assume that the company still holds assets that can be liquidated. If the company has only debts and no assets, a fast-track liquidation is the only viable course of action. Furthermore, in this guide we assume that in the first phase, the board has already assessed the possibilities of debt restructuring (potentially through a WHOA procedure) and exhausted all financing options.

The process begins with the board informing the general meeting of shareholders about the financial situation, explaining why, in its view, there is no longer a prospect for long-term value creation or even survival, and advising that a bankruptcy is the appropriate course of action. Based on this advice, the board should request the general meeting to issue instructions authorizing the board to file for bankruptcy. Once the board receives this instruction, it may, at its discretion, resolve to proceed with the bankruptcy filing.

Subsequently, the company must complete the required forms and submit the necessary supporting documents. After a hearing, the court will generally approve the application and declare the company bankrupt, with retroactive effect to midnight on the day of the hearing. The court will also appoint a bankruptcy trustee, who is responsible for the proper administration and settlement of the bankruptcy estate. The board and any members of the supervisory board are legally required to fully cooperate and provide all requested information to the trustee. It is advisable to prepare all relevant financial and operational documentation in advance of the bankruptcy filing, so that the trustee can immediately assess the situation and explore the possibility of a restart of the business.

If the general meeting does not grant the requested instruction to apply for bankruptcy, filing without such authorization carries a significant risk of director liability and is therefore not recommended. In such cases, the more appropriate course of action is often for the board to apply for a suspension of payments (surseance van betaling), which does not legally require shareholder approval. In this scenario, the court will appoint an administrator (bewindvoerder) to guide the company through the process. The goal of a suspension of payments is to facilitate the company’s continued existence and avoid bankruptcy. However, in practice, it often ends with the administrator determining that there is no realistic prospect of recovery and requesting termination of the suspension. The court will then typically declare the company bankrupt. In other words, suspension of payments may serve as another pathway to bankruptcy.

Before carrying out these steps, the board should again carefully assess whether there are any contractual obligations that affect this process. For example, shareholders’ agreements often include provisions requiring that the board obtain approval from the general meeting before applying for suspension of payments. Furthermore, filing for bankruptcy or suspension of payments, or even the intention to do so, may trigger notice, covenant, and default provisions in financing documents.

5. PRACTICAL TIPS

When a company faces financial difficulties, it enters into a new and often stressful playing field. Investors are unhappy that their investment may go up in smoke, creditors are unhappy that they may remain unpaid, and employees are unsure about their future employment. Furthermore, directors have the added stress of facing the risk of personal liability. The following tips aim to provide practical guidance to directors in order to navigate these circumstances.

Maintain an accurate, detailed, and up-to-date financial administration so that the company’s financial position is always clearly known. The scope of this administration depends on the nature and size of the company, but it must at minimum provide insight into the company’s debts, receivables, and liquidity position. Proper administration is essential for good decision-making in times of financial distress and for keeping the supervisory board, general meeting, and potentially a bankruptcy trustee adequately informed. Moreover, this obligation is imposed by law, and failure to comply significantly increases the risk of directors’ liability in the event of bankruptcy.

Continuously analyse the company’s financial position and prepare financial forecasts. It is essential for the board to remain aware of whether it is still realistic that the company has future prospects. Ideally, the forecasts should include different scenarios, such as a 'management case', a 'bank case', and a 'worst-case’ scenario. Having these scenarios allows the board to respond quickly and adequately if the circumstances change, for example if an outstanding investment application is rejected. Furthermore, it helps the board in justifying its decisions and keeping the supervisory board and general meeting properly informed.

Ensure timely filing of the annual accounts. Failure to comply with the statutory obligations to maintain proper financial administration or with obligations in relation to the annual accounts constitutes improper management and increases directors’ liability risks if the company goes bankrupt. While these statutory obligations always apply, they become particularly critical in times of financial distress due to the heightened risk of insolvency.

Be aware of the content of key documentation, such as governance documents (shareholders’ agreements, voting agreements, articles of association) and financing arrangements and other key agreements. The company’s financial situation may trigger provisions in these documents, such as covenants or default clauses in loan agreements. Additionally, they may contain approval requirements or information rights that are directly relevant to the actions the board intends to take.

Keep records of all relevant developments, board resolutions, and envisaged actions. As set out above, the board must balance the interests of all stakeholders and be able to justify its resolutions and actions. To do so, it should regularly hold board meetings to discuss recent developments, deliberate on strategy, adopt resolutions, and decide on appropriate actions. How frequently board meetings should be held depends on the nature and size of the business, but in our experience, it is good practice to have at least one per week that is well documented. The minutes of these meetings should clearly reflect why the board considers its decisions justified, based on the company’s financial position, forecasts, and stakeholder interests. The paper trail of these minutes is crucial in defending the board’s actions in any future liability disputes. Smaller businesses often do not hold formal board meetings, for example because responsibilities are divided informally between directors or because the company has only one director. Even in such cases, we recommend introducing regular, formal decision-making moments for the reasons set out above. Where there is only one director, these may take the form of structured consultations with senior management or external advisers, such as outside counsel, with proper documentation of the considerations and decisions made.

If the company has D&O insurance (directors and officers liability insurance) and has paid its premiums, timely notify the insurer of any potential claims. It is essential to inform the insurer as early as possible about any potential future claims. Failure to do so may lead to coverage disputes. Consult the insurance policy for the specific notification procedure.

Engage professional help, such as a restructuring expert and legal counsel. Directors must assess whether they have the expertise to guide the company through financial distress. If not, they are expected to engage qualified external advisors to properly assess the scenarios and assist with key decisions. As noted above, it is often in the interest of the company and its joint creditors to incur the costs of external advice, potentially making it a justifiable expense.

Exercise great caution with regard to transactions with affiliated parties or that are not at arm’s-length terms. In financially distressed situations, such transactions may harm the interests of creditors or other stakeholders and are likely to be scrutinised by a bankruptcy trustee. These transactions carry a substantial risk of annulment or liability disputes. If the transaction is in the best interest of the company and its collective creditors, ensure that correct governance procedures are followed and that the commercial rationale is thoroughly documented.

Involve stakeholders and corporate bodies in the decision-making process. Seeking input from the supervisory board, key shareholders, and the general meeting can bring valuable perspectives to difficult decisions and can help directors in sharing the load (although remaining responsible). Engaging external parties, such as banks or major suppliers, early and transparently helps mitigate liability risks and may increase support for a possible restart following bankruptcy. Involving stakeholders early also has the added benefit that they may be able to support the company financially.

6. NEXT STEPS

Guiding a company through financial distress requires swift and acute but also diligent and considerate actions from the board. The good news is that if a director does so within the confines of the law and considering the interest of the company and its stakeholders, the risks of personal liability can be mitigated.

The lawyers of full-service firm De Roos have the right expertise to help any entrepreneur navigate the complexities of this legal landscape. Are you a director of a company that finds itself in financial difficulty, or are you a stakeholder in a company that is in this position, and do you want to know your options? Please do not hesitate to reach out.