When an SPA is void: a practical guide to getting shares “back”

Voidance operates retroactively, yet it does not automatically unwind the notarial transfer of registered shares. This guide outlines why a return deed is required, what can go wrong without it, and what boards should do while ownership is disputed.

By Sjoerd Buijn

Expertise:

Corporate Notarial

22.05.2026

When shares come back: Why nullification of an SPA is not enough

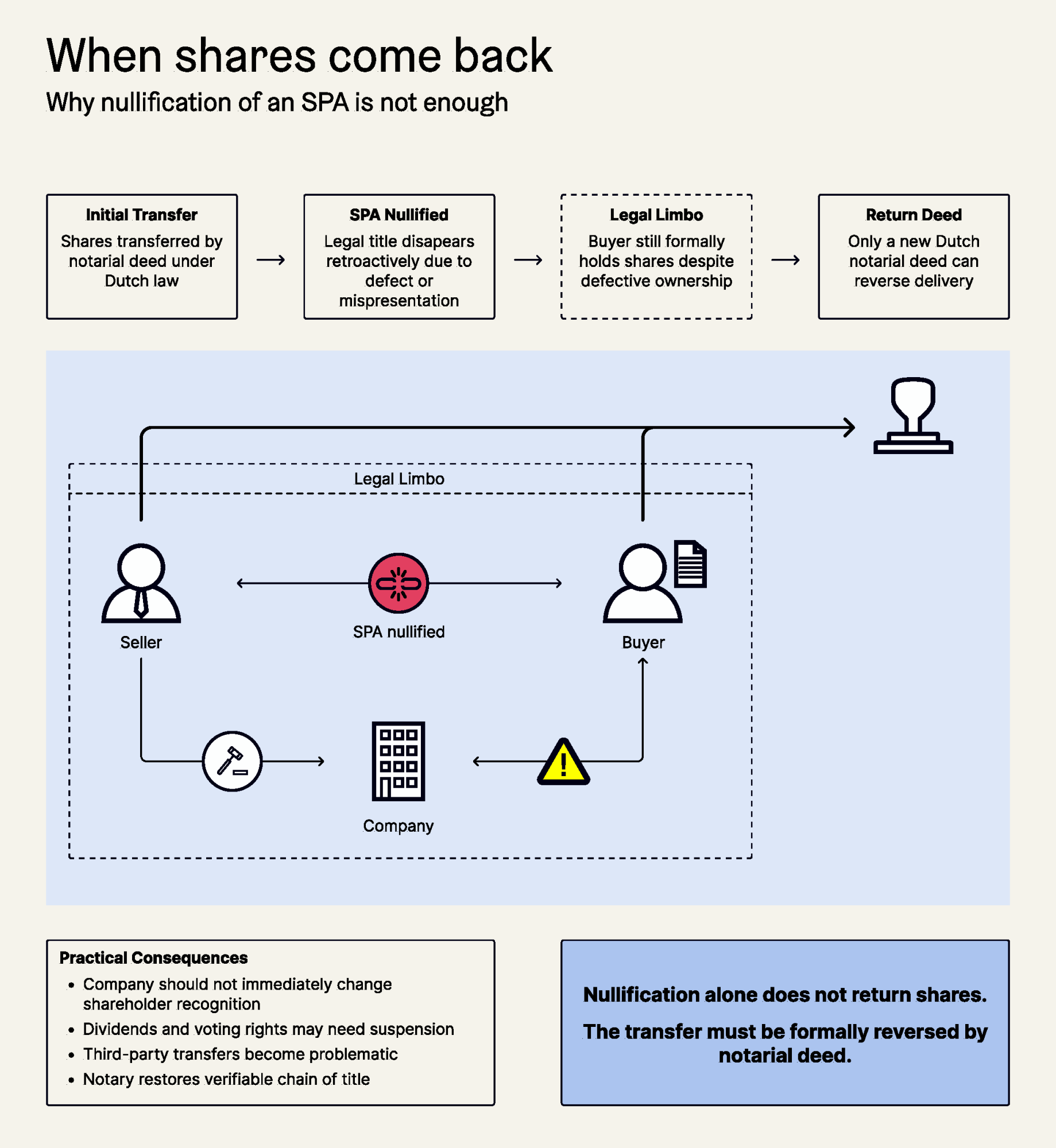

Imagine you buy a book, and it later turns out the seller misrepresented what they were selling. You void the deal, hand the book back, and get your money. Simple. But what if you had bought shares instead? And what if nullifying the purchase agreement were not the end of the story, but only the beginning of a more complicated legal journey?

That is exactly the situation that arises when a share purchase agreement is voided due to a title defect. And the answer, perhaps counterintuitively, is that simply declaring the deal null and void does not automatically return the shares to the seller. A formal notarial deed of return is required — and without it, the parties, the company, and third parties are left in a legal no-man's land.

How share transfers work and where they can go wrong

Under Dutch law, transferring ownership of an asset requires three things: delivery, a valid legal title (reason for the transfer), and authority to dispose of the asset. When a purchase agreement is voided, for instance because the seller misrepresented the company's financial position, the title disappears, retroactively, as if it never existed. In property law terms, the shares are deemed never to have left the seller's estate.

This sounds reassuring: if the transfer never legally happened, surely the seller is already back where they started? Not quite. The delivery itself, the notarial deed by which the shares were transferred, did validly take place. The buyer becomes what Dutch law calls an unauthorised holder: someone who holds the shares without a legal basis. The shares may, in theory, still belong to the seller — but the seller cannot simply act as if they never changed hands. Like the book that needs to be returned, the shares will have to be returned.

Why a notarial deed of return is essential

The delivery of registered shares under Dutch law can only take place by means of a notarial deed executed before a civil-law notary in the Netherlands. This is not a formality, it is a constitutional requirement. And the same requirement applies in reverse: to undo the delivery, a new notarial deed must be executed.

This matters in practice. Without a formal deed of return, the seller cannot validly transfer the shares to a third party. You cannot deliver something while another person is still holding it, even unlawfully. The chain of title is broken, and the notary's ability to verify legitimate ownership at each step, the so-called title search, is compromised. In cases of extrajudicial nullification (where no court has ruled, and a party simply invokes nullification by letter), the absence of a return deed leaves a significant gap in the documentary trail that the legislator specifically designed the notarial system to prevent.

What this means for the company

The consequences extend beyond the buyer and seller. The company itself, which distributes dividends, facilitates voting at shareholder meetings, and maintains the shareholders' register, is caught in the middle.

A company that receives a unilateral declaration of nullification by post is not obliged to immediately recognise the original shareholder again. Nor should it be. The shareholders' register, while it should reflect reality, has no constitutive (property law) effect: the fact that it lists someone as shareholder does not mean the shares have been formally returned to them. Updating the register is not a substitute for the return deed.

Until a notarial deed of return has been executed and communicated to the company, the company is best advised to continue treating the buyer as the shareholder for corporate governance purposes. Where the nullification is disputed or uncertain, it is prudent to suspend dividend payments and voting rights for the shares in question, directing the parties to resolve ownership through the courts if necessary. This protects the company from being drawn into a title dispute that is not of its making.

The notary as gatekeeper

The notarial deed of return serves a dual function. It restores the correct legal position between buyer and seller: re-establishing the original ownership relationship. But it also creates an objective, externally verifiable turning point for the company and other third parties.

Importantly, a notary cannot responsibly execute a return deed without involving both parties and satisfying themselves that the restoration of the original position is defensible. This built-in due diligence is a feature, not a formality. It provides a safeguard against one party unilaterally asserting a change of ownership that the other contests.

The return deed should also address the financial footprint left by the period of (legally speaking, defective) ownership. Dividends distributed during that period should, given the retroactive effect of nullification, ultimately accrue to the seller. Share-related allocations, such as bonus shares or share premium-related issuances, should be addressed in the return documentation. More complex situations, such as shares acquired through pre-emption rights or blocking mechanisms during the contested period, will typically require bespoke arrangements.

The broader lesson

The legal vacuum created by nullifying a share transfer title is real. Property law establishes that the shares never legally left the seller, but it does not, by itself, undo the physical and legal shift that took place when the notarial deed of delivery was executed. That shift requires a corresponding deed to reverse it.

A system where shares are assumed to "automatically" return to the seller upon nullification without any formal deed would undermine the very purpose of the notarial chain: to provide transparent, verifiable, and reliable evidence of who owns what at every point in time. For sellers who believe they have a strong nullification claim, the practical message is clear: do not stop at the declaration. Complete the return by deed. For companies facing shareholder disputes of this nature, the message is equally clear: wait for the notarial deed before recognising any change in ownership — and in the meantime, manage the uncertainty carefully.